Changes to social insurance and salary

Changes to social insurance and salary

Social security is an emotive issue, as can be seen in the number of referendums, the worry barometer and (social) media. We will keep you up to date on what needs to be considered in the coming year.

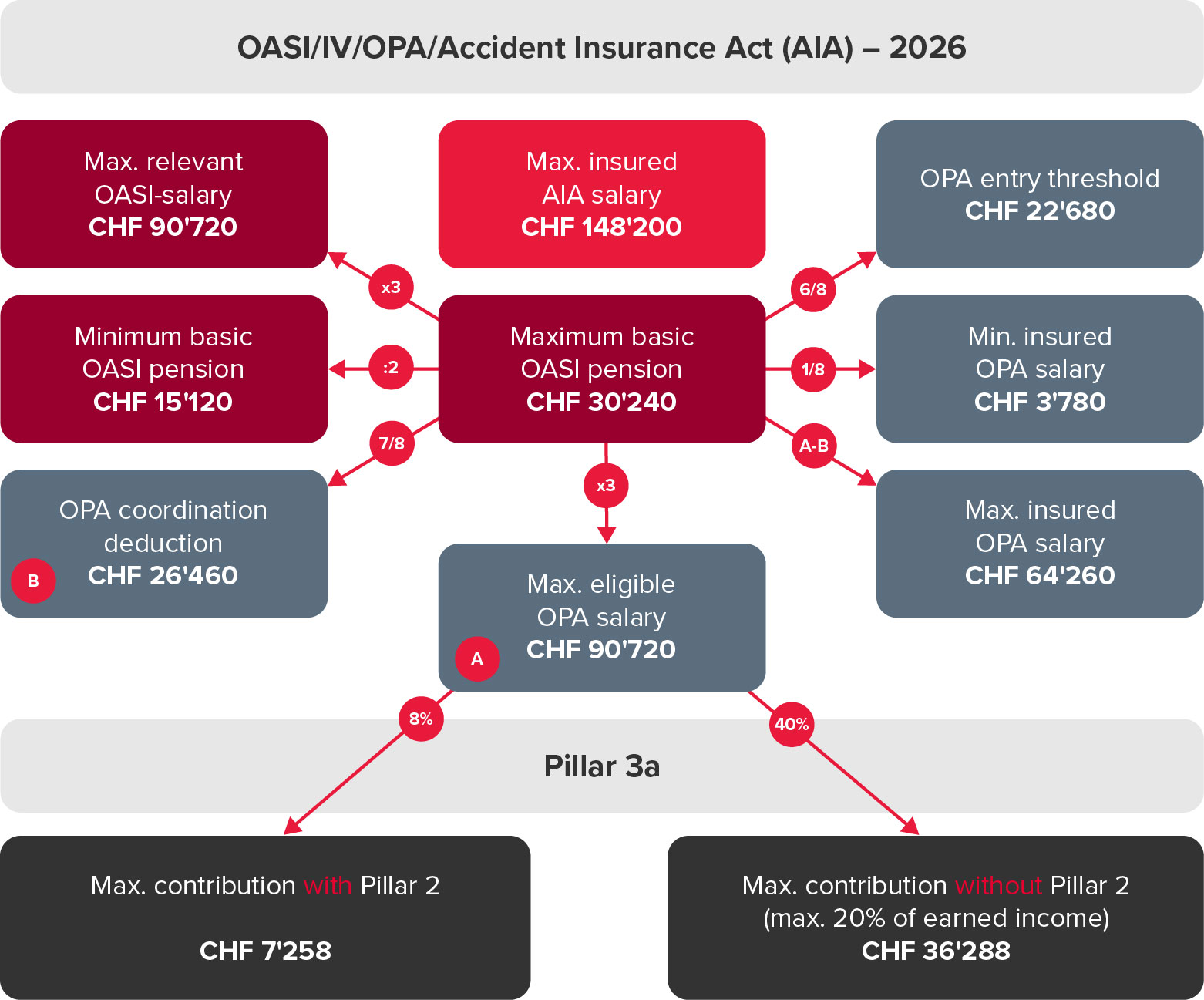

Limits, key figures and contributions 2026

The OASI maximum pension will not be adjusted for the new year, meaning that all Occupational Pensions Act (OPA) and Pillar 3a limits will remain at the same level. You can download our popular flyer with the latest social security contributions for 2026 via this this link.

OASI

In addition to the adjustments to the new tax practice explained below, there are the following innovations and clarifications.

13. Rente

The 13th pension will be paid for the first time in December 2026. This is treated as a surcharge, as can be seen from the unchanged thresholds. It is not taken into account when calculating the pension supplement for women in the OASI 21 transition generation, parental or carers' credits or thresholds based on the minimum or maximum OASI pension. It does not lead to a reduction in supplementary benefits. The 13th pension is also not factored in when determining the ceiling for married couples (limiting individual OASI pensions to a total of 150% of a maximum pension), but it is calculated based on the pension reduced by the ceiling.

Anyone entitled to an OASI pension on 1 December will receive the 13th pension. There is no pro rata entitlement in the event of death before 1 December. The same applies if the pension entitlement lapses due to moving away or widowhood before 1 December. The compensation offices must obtain a life certificate from the entitled person before making the payment.

In the event of changes to the OASI pension during the year (new start, recalculation on request, recalculation after splitting - 50% allocation of income earned during the marriage in the event of divorce, widowhood or if both spouses have reached the reference age), the 13th pension is calculated as the average pension paid during the year. The 13th payment only applies to retirement pensions, not disability, widow’s and widower’s, child and supplementary benefits.

In the case of an early withdrawal, the 13th payment is also reduced. Once a deferred pension is taken, the 13th payment is paid out including deferral surcharge.

Compensation offices will directly inform beneficiaries about the calculation and payment methods during 2026, by the first payment at the latest. An appealable ruling will be issued upon written request.

Women’s retirement age

With the implementation of OASI 21, women born in 1962 will reach retirement age at 64 years and 6 months.

Negligible salary

If an employee earns no more than CHF 2,500 per year, OASI contributions only have to be deducted at the employee’s request. However, this exemption does not apply to some occupational groups, meaning that salary must be deducted from the outset. Previously, this involved salaries of employees in private households or in the arts and culture sector. It now also applies to employees in museums, design companies and in electronic and print media.

Net salary compensation

The Guidelines on base salary (WML)1, specify in paragraph 2084 what was already applicable: with continued salary payment and net salary compensation, only the reduced continued pay is relevant. The net wage adjustment must therefore be made to gross salary, not just the amount paid.

Allocations for basic and advanced education and training

The WML adopts the note from the Swiss Tax Conference (Schweizerische Steuerkonferenz – SSK) FAQ on wage statements that the assumption of costs for training already completed is deemed to be an employer benefit on starting employment. Whether this is also a salary subject to AHV contributions depends, among other things, on the connection with the professional activity.

Asymmetric dividends

If people are both employees and shareholders in a company, the question arises as to how wages (remuneration for labour, subject to social security contributions) and dividends (capital gains, not subject to social security contributions) are to be split. In addition to the rule that dividends exceeding 10% of the taxable enterprise value are deemed excessive, in the case of asymmetric dividends, the portion that remunerates work performed should now be eliminated in a first step. Only at the second stage is the excessive dividend examined in relation to the appropriate salary. Case law is thus adopted in the guidance (para. 2018.1 WML).

Family allowances

Cantonal child and education allowances will rise to CHF 240 and CHF 290 respectively in Graubünden and to CHF 225 and CHF 278 respectively in Aargau. In various cantons, family allowance contributions are also rising or falling.

Loss of earnings compensation (EO)

Paper-based EO registration will be abolished. In future, people serving in the army, civilian service, civil protection and “Youth and Sport” will submit their applications digitally. Other EO benefits are not affected. The digital process will be introduced in stages from early 2026. Compensation offices will collect the information required from employers via a letter with a QR code, an existing online portal or via a direct connection to an ERP system. Notifications that were still paper-based before the changeover will be handled via the usual process.

Short-time working compensation (KAE)

Within the framework period for receiving benefits (two years), companies affected can receive KAE benefits for a maximum of 12 months. The Federal Council may extend the maximum entitlement period to 18 months. In September 2025, the law was amended as a matter of urgency so that the Federal Council can extend the maximum entitlement period to 24 months, which it did on 1 November 2025. This means that KAE can be drawn for up to two years until 31 July 2026; this also applies to existing framework periods. This is intended to provide even better support for companies whose order books are suffering from the additional US tariffs. The legislation applies until 31 December 2028.

Pillar 3a

For the first time, people who have not made the maximum possible payments in 2025 will be able to do so in 2026. You can find out more in this article Purchases for Pillar 3a will be possible from 2025 - BDO.

Salary statements and expense regulations

The Federal Tax Administration has amended the instructions for completing the salary statement in certain areas. Among other things, the cost rate per kilometre was increased from 70 to 75 centimes. This has various effects:

Compensation for business trips with a private vehicle

The maximum permissible kilometre allowance for business trips with a private vehicle is now 75 centimes. For employees who frequently use their private car for business trips, the template of the Swiss Tax Conference (SSK) has been in force since 1 May 2024. Inconsistently, these flat rates have not been adjusted to date. The template can be downloaded here: Sample templates for expense regulations for companies and NPOs. Expense regulations approved by the employer’s canton of domicile are recognised by other cantons, provided the template guidelines are followed.

A cross must now be placed in field “F” on the salary statement when car allowances are paid in accordance with the above-mentioned template. This makes it clear that employees receiving this cannot claim a professional expense deduction for travelling to work.

The increased kilometre allowances are also considered expenses for OASI purposes and no contributions are owed on these. As the new template for flat-rate allowances stipulates that employers must provide evidence of the kilometres driven on business over a representative time period, corresponding records can be requested during an employer inspection – in spite of approved expense regulations.

Whether the kilometre allowance is actually increased for employees is at the discretion of the employer. This is a maximum value in order to prevent excessive expense allowances. However, it is permissible to pay out lower compensation.

Personal use of business vehicles

There is no change to the flat-rate regulation for personal use of business vehicles. However, invoicing of personal shares can only be waived if employees are charged the new rate of 75 centimes per kilometre for personal use.

Abolition of REKA checks

No new REKA checks will be issued from 2026. While the REKA check rule in the salary statement guidelines no longer applies, benefits are now also possible and generally regulated for other services – more on this in the next section “New CHF 600 limit”.

New CHF 600 limit

Employers can pay their employees benefits in accordance with the following table without having to declare them on their salary statement. In addition to the increase in the amount, the more restrictive OASI regulation with a limit on the annual amount was also adopted for taxes.

| What | Max. value | Exceeding value | Change on 2025 |

|---|---|---|---|

| Discounts for products and services | 20% per benefit, up to a maximum of CHF 600 per year | Exceeding value: Declare in section 2.3 and Max. effective OASI salary | New regulation |

| Usual gifts in kind | Max. CHF 600 per calendar year | Whole amount: Declare in section 2.3 and Max. effective OASI salary | • Increase from CHF 500 to CHF 600 • now per year instead of per event (analogous to OASI) |

| Admission cards for events | Max. CHF 600 per calendar year | Exceeding value: Declare in section 2.3 and Max. effective OASI salary |

Fire brigade pay

Under certain conditions, the pay of volunteer firefighters is exempt from tax and OASI contributions. The limit will be increased from CHF 5,300 to CHF 5,400.

Cross-border employment relationships

The provisions of the Guidelines on compulsory OASI/IV insurance (WVP)2 have been relaxed with regard to so-called “workation postings” (temporary cross-border teleworking in a country other than the country of residence or employer). Previously, secondments abroad with continued social security coverage in Switzerland were only possible if they were in the interests of the employer. Compensation offices can now also authorise workation in a contracting state if there are compelling personal reasons (medical reasons, caring for relatives or accompanying a spouse who has been posted). The duration of such a secondment may not exceed the duration set out in the agreement.

Workation in the sense of multiple employment with regularly recurring activities in another country for personal reasons is still not regulated.

Conclusion and outlook

In view of the forthcoming changes, business will remain exciting in 2026. The Federal Council has presented an initial proposal for the OASI 2030 reform. Some measures are intended to generate additional income (daily allowances now subject to contributions, further tightening of the salary/dividend issue, higher contributions for the self-employed). Others are intended to encourage work beyond the official retirement age (higher pensioner’s allowance, adjusting supplements or reductions for pension deferral or early withdrawal, increasing pensions via a multiplier in the salary credit from the reference age). The idea of raising the minimum age for early retirement in the Pillar 2 from 58 to 63 is also likely to be controversial. Politicians also want to make social insurance more independent of marital status.

Stay informed with us: we are here for you, with training courses, newsletters and direct individual advice. Take advantage of our expertise and experience. We look forward to seeing you!

1 Guidelines on relevant salary for Swiss old-age and survivors’ insurance (OASI), invalidity insurance (IV) and loss of earnings compensation (EO), valid from 1 January 2019, as at 1 January 2026

2 Guidelines on compulsory OASI/IV insurance, valid from 1 January 2009, as at 1 January 2026

Do you have questions about social insurance? Our team is here to help.

LEARN MORE ABOUT OUR SERVICES